In today's unpredictable world, having an emergency fund is a cornerstone of sound personal finance for families in India. It acts as a financial safety net, helping you navigate unexpected expenses without derailing your long-term investment goals. While global financial experts often recommend saving 3-6 months' worth of living expenses, in the Indian context—considering factors like job market stability, healthcare costs, and family obligations—building this fund is even more crucial. However, starting with a more achievable target can encourage common investors to begin sooner rather than feeling overwhelmed.

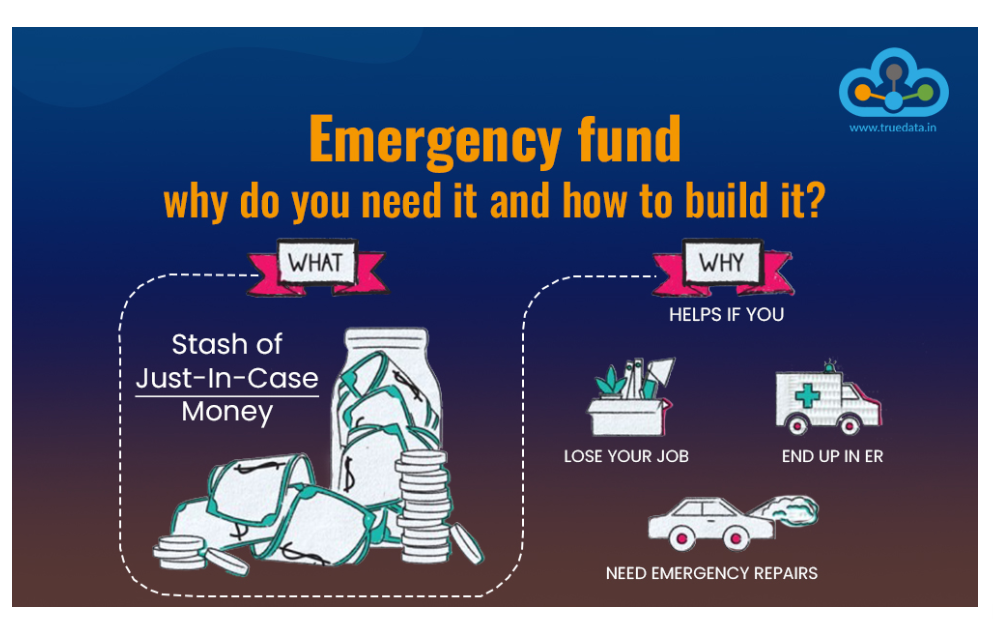

Why Build an Emergency Fund?

An emergency fund provides peace of mind and protects against life's uncertainties, such as medical emergencies, job loss, or urgent home repairs. Here are key benefits:

-Avoids High-Interest

Debt:

Without a fund, you might rely on credit cards or personal loans, which

carry high interest rates (often 15-40% in India), leading to a debt trap.

-Handles Short-Term

Volatility: It

helps manage temporary cash flow issues, like delayed salaries or

inflation spikes, without touching long-term investments like mutual funds

or stocks.

-Protects Long-Term

Goals: By

not liquidating investments during market downturns, you preserve compound

growth potential for goals like retirement or education.

-Promotes Financial

Discipline:

Building and maintaining the fund encourages budgeting habits and reduces

impulsive spending.

-Offers Quick Access in

Crises: Bureaucratic

delays in insurance claims many need immediate cash availability is vital.

Recommended Amount in the Indian Context

The standard advice is to aim for 6-12 months of essential expenses as an emergency fund, accounting for India's economic volatilities like job insecurity in sectors such as IT or manufacturing. However, for beginners or common investors, starting with 4 months' worth can be sufficient and less daunting—especially if you have a stable job, health insurance, and family support. This excludes your current month's expenses. Calculate it based on must-haves like rent, groceries, EMIs, and utilities (e.g., if monthly expenses are ₹50,000, target ₹2 lakh initially).

Where to Park Your Emergency Fund

To balance liquidity, safety, and modest returns:

Savings Account (1

Month's Expenses): Keep

this in a low-interest savings account (yielding 3-7% annually in India)

for instant access via ATM or UPI.

Liquid Funds (3 Months' Expenses): Invest in low-risk liquid mutual funds, which offer better returns (around 6-7%) than savings accounts, with same-day redemption options up to ₹50,000. Popular options include funds from HDFC, ICICI, or Nippon India, invested in short-term debt instruments.

Without an Emergency Fund – Raj's Struggle

Raj, a

35-year-old IT professional in Bengaluru earning ₹80,000 monthly, lived

paycheck-to-paycheck, investing most savings in stocks for quick gains. When he

lost his job during a company layoff amid economic slowdown, he had no buffer.

Desperate for cash to cover rent (₹25,000) and family expenses, Raj sold his

equity investments at a 20% loss during a market dip. He also took a personal

loan at 12% interest to bridge the gap, adding ₹10,000 in monthly EMIs. It took

him two years to recover financially, delaying his home purchase dream. This

highlights how lacking a fund forces poor decisions, amplifying losses.

With an Emergency Fund – Priya's Resilience

Priya, a

32-year-old teacher in Mumbai with ₹60,000 monthly income, had built a 4-month

emergency fund: ₹60,000 in her savings account and ₹1.8 lakh in a liquid fund.

When her mother needed urgent surgery costing ₹1.5 lakh (partly covered by

insurance, but with upfront payments), Priya withdrew from her fund

seamlessly—no loans or investment sales needed. She redeemed from the liquid

fund instantly, earning a small return in the process. Within months, she

replenished the fund by cutting non-essentials. This buffer not only covered

the crisis but protected her SIPs in equity funds, which grew 15% that year.

Priya's story shows how an emergency fund provides stability and safeguards

wealth-building.

Start small

today—track your expenses, automate savings, and review annually. An emergency

fund isn't just money; it's freedom from financial stress.

ArthaMantra Investments is an independent financial services firm based in Pune, India.

ArthaMantra Investments is an AMFI Registered Mutual Fund Distributor.

Disclaimer: Mutual fund investments are subject to market risks. Please read the scheme information and other related documents carefully before investing. Past performance is not indicative of future returns. Please consider your specific investment requirements before choosing a fund, or designing a portfolio that suits your needs.

ArthaMantra Investments makes no warranties or representations, express or implied, on products offered through the platform of ArthaMantra Investments. It accepts no liability for any damages or losses, however, caused, in connection with the use of, or on the reliance of its product or related services. Terms and conditions of the website are applicable. Investments in Securities markets are subject to market risks, read all the related documents carefully before investing.